Rising Medical Loss Ratio is one of the most pressing challenges facing Medicare Advantage plans today. With shrinking margins, rising utilization, and increasing regulatory scrutiny, many plans feel the pressure to act fast.

The most common responses are predictable and, intuitively, they make sense:

- Tighten utilization management

- Revisit provider controls

- Push harder on cost containment programs

These actions are logical, necessary, and they are part of every well-run Medicare Advantage organization.

Unfortunately, for many plans, they are also insufficient. That’s because high MLR is often not just a cost problem but a revenue alignment problem hiding in plain sight.

Why MLR Pressure Feels So Relentless

At its core, MLR is a simple ratio. Medical claims expense divided by premium revenue. What makes it so volatile is how sensitive profitability is to even small changes in that ratio.

Consider a plan operating at 85% MLR with a modest profit margin. A one percent (1%) increase in MLR does not reduce profit by one percent. It potentially reduces profit upwards of 30% or more. That’s the reality many plans are living with today.

Further compounding the problem, most revenue inputs are not flexible in-year because benchmarks are set, premiums are locked, and STAR timing is fixed. When costs rise faster than expected, plans feel trapped with very few levers that can move quickly.

That is why cost containment becomes the default response. But this focus often overlooks a critical question.

Is the plan being paid accurately for the risk it is already managing?

Why Averages Hide the Real MLR Problem

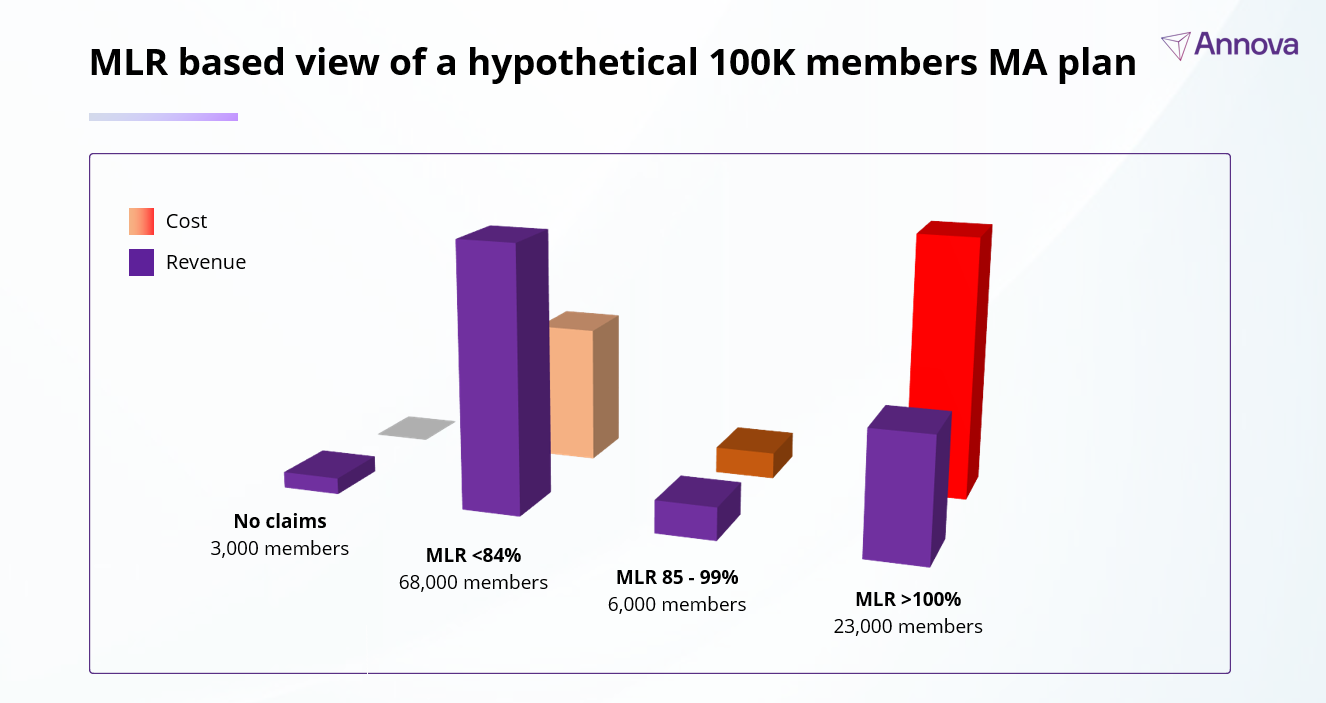

One of the biggest mistakes plans make is only looking at MLR at the aggregate level. Averages tend to smooth over—obscure, really—what is happening inside the population.

When MLR is viewed through population segmentation, a very different picture emerges. In a typical Medicare Advantage population, members fall into a few broad groups:

- Members with no claims

- Members with low MLR whose care is highly cost-effective (i.e., “profitable”)

- Members with moderate MLR

- Members with MLR greater than 100%

Most plans instinctively focus on the last group. The assumption is straightforward: these members must be driving excessive cost because they’re overutilizing resources. Clearly, they must be the problem, right?

Not exactly. The data tells a more nuanced story.

If you look closely at high-MLR populations, chances are you’ll find these members are “expensive” on paper not because the cost of treatment is higher but because their risk is under-captured.

Across multiple plans and markets, population level analyses suggest that 30% to 50% of members in high MLR cohorts do not have risk scores that fully reflect the severity and complexity of their conditions.

These members are clinically complex, and their real care generates real claims. However, the revenue associated with their disease burden is incomplete.

The result is a structural mismatch. The plan pays for care but is not fully compensated for the risk it’s already managing. MLR rises, even when utilization patterns are reasonable.

This is where many MLR strategies quietly fail.

Before reducing spend, plans need to make sure they are being paid accurately for the risk they’re carrying.

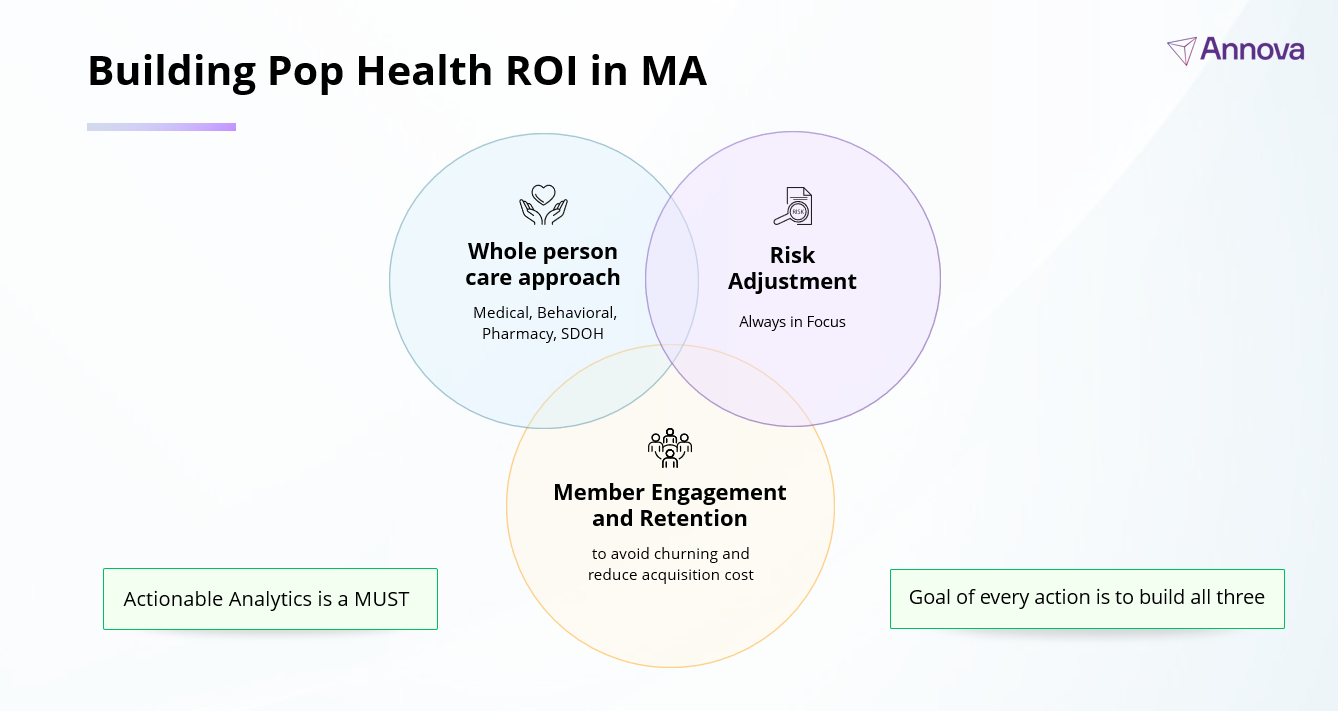

The Three Levers That Actually Shape MLR Outcomes

Strong Medicare Advantage performance rests on three interconnected levers:

- Cost containment and member health. Care management, utilization management, and provider engagement work in tandem to drive the cost of care.

- Member engagement. Members who are engaged in their care are more likely to stay with the plan, adhere to treatment, and avoid preventable deterioration.

- Finally, for better or worse, funding levels directly shape MLR. That funding comes from accurate risk adjustment.

Too often, plans invest heavily in the first two levers while underinvesting in the third. When funding is weak, the rest of the care delivery system pays the price. Care management programs become harder to sustain, engagement efforts lose momentum, and MLR pressure compounds year over year.

Why Utilization Management Alone Cannot Solve the Problem

Utilization management remains an important tool. But its impact has limits.

Medical trend continues to rise year over year. Regulatory oversight constrains how aggressively utilization can be managed. Many cost control strategies take years to fully materialize. Even best-in-class utilization programs struggle to offset structurally under-captured revenue.

When the revenue side of the equation is misaligned, cost discipline alone cannot restore margin stability.

How MLR Should Be Approached: A Needed Shift

The fastest path to sustainable MLR improvement is not spending less on care for members. It is ensuring the plan is paid correctly for the care it is already providing.

This requires a shift in mindset. Risk adjustment should no longer be treated as a downstream activity but recognized as a core financial and population health discipline. Quite simply, risk adjustment isn’t just a coding exercise—it’s financial engine that enables population health to exist at scale.

Plans that align revenue with true disease burden create room to invest in care, member and provider engagement, and long-term outcomes without destabilizing margins.

Given the threat of reduced benchmarks impacting already razor-thin margins, that alignment is no longer optional. It is foundational.

Stop chasing utilization and start capturing risk. Learn how Annova’s data-driven approach aligns your revenue with the true clinical complexity of your members.

Schedule a quick, no-pressure call with our experts today to discuss your population segments and identify where your revenue might be hiding in plain sight.